[ad_1]

The 12 months 2024 left many difficult in addition to optimistic approaches, particularly for the gear industries. On the one hand, the demand for gear is skyrocketing because of the fast initiatives of infrastructure and residential constructing building, whereas then again, the costs of heavy gear are going past the attain of the consumers, making them resist investing in heavy-duty machines.

On this unsure state of affairs, the OEMs try their finest to convey extra user-friendly offers to assist the consumers. It’s fairly necessary to maintain a strict eye available on the market traits for all of the consumers and stakeholders.

How did the market appear like in December 2024?

All of the people related to the gear trade for any purpose, know that the trade has skilled some noticeable change up to now few years. There are a number of causes for this fluctuation together with the rising gas costs, and unstable financial and political conditions.

Regardless of all this, understanding the fluctuating market traits will enable you to make smart judgments whether or not you’re accountable for heavy-duty or medium-duty gear.

The medium-duty gear market is in keeping with minor fluctuations

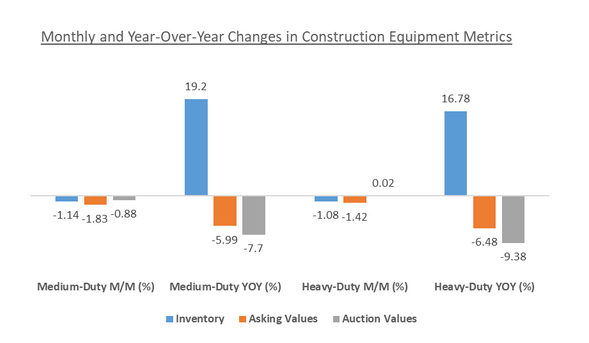

Medium-duty building gear is at all times in demand and therefore its stock degree is majorly affected.

Nevertheless, in December 2024, it noticed a decline in month-over-month (M/M) gross sales by 1.14%, whereas the Yr-over-Yr (Y/Y) gross sales elevated by 19.2% which is likely one of the most superb knowledge to notice.

If we speak concerning the skid steer stock, the fluctuation was recorded by 3.33% M/M in a declined sample and a rising sample in Y/Y by 29.17%. The professional states that this means the demand for this class of kit remains to be intact and never going anyway down within the few subsequent years.

Within the meantime, asking values have been declining. They fell 1.83% month over month and 5.99% 12 months over 12 months in November, with used backhoe loader on the market struggling the most important dip at 3.48% month over month.

Comparable downward traits had been seen in public sale values, which fell 7.7% 12 months over 12 months and 0.88% month over month.

Whereas, loader backhoes as soon as once more noticed the most important decline, down 3.35% M/M. At 12.38%, wheel skid steers noticed the most important year-over-year drop in public sale values, indicating a tough marketplace for sellers however a beneficial one for consumers.

The heavy-duty gear section has seen main fluctuations

In November, the marketplace for heavy-duty gear gave some unsure and conflicted patterns. Stock ranges are nonetheless 16.78% larger 12 months over 12 months, regardless of a minor M/M discount of 1.08%.

Surprisingly we’ve seen a significant shift within the wheel loader class with virtually 32.03% Y/Y rise in inventories whereas a decline in M/M by 2.05%. It’s a clear indication that the availability of this class of kit is larger available in the market which can put additional stress on sellers to once more change the costs.

Crawler excavators confirmed sturdiness on this section, as seen by their 2.7% M/M improve in public sale values.

Wheel loaders, then again, noticed the most important year-over-year decline in public sale worth (10.5%), suggesting that this class could present some offers, nonetheless, issues are nonetheless unsure.

[ad_2]

Source_link